In order to get full access to this article, email us at thedocumentco@hotmail.co.uk

Ref No: 4051

Table of Contents

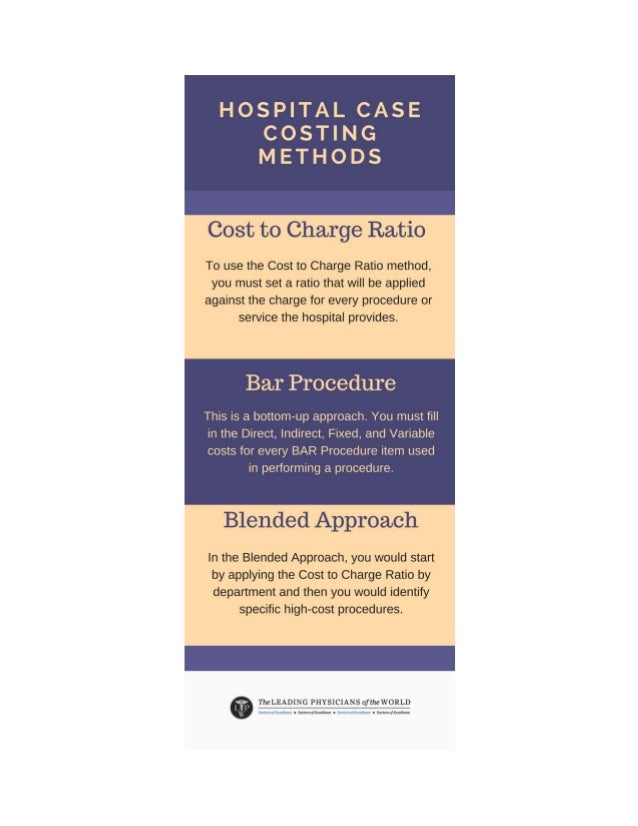

Healthy Hospital Costing Techniques

Advantages and Disadvantages of changing the costing system.

Alternative Adoptable Pricing Strategies

This report is a detailed analysis of Healthy Hospital’s Costing Techniques. It mainly draws comparison between traditional costing method and activity based costing method. This report will then take into account the pricing strategies that maximizes profitability.

This report will also help the reader take informed decisions about any alternative potential pricing strategies

There are two elements of cost. One is direct cost and the other one is indirect cost.Direct cost is apportion directly. Therefore, no change will occur whichever method is used. Indirect costs are according to total number of budgeted operations.

Feet Knee Hip

| Sales Per Operation | 3000 | 4000 | 4400 |

| Less Cost | 2770 | 3290 | 3300 |

| Profit | 230 | 710 | 1100 |

| Total Profit | 2040 | ||

| Profit Margin: Per £ | 0.0767 | 0.1775 | 0.2500 |

| Profit Margin: % | 7.6667 | 17.75 | 25.000 |

*See Details in Appendix

Net profit margin represents net profit to costs percentage. It is a good overall view of the activities.In identical industries, net profit margin can tell which company is performing better.(Bragg, 2018)

The total direct costs of operations remain the same. However, the indirect costs change dramatically.The director ordered to allocate indirect costs to total number of operations.

Feet Knee Hip

| Sales Per Operation | 3000 | 4000 | 4400 |

| Less Cost Per Operation | 2514.00 | 3374.48 | 3480.51 |

| Profit | 486 | 625.52 | 919.4872 |

| Total Profit | 2031.007179 | ||

| Profit Margin: Per £ | 0.162 | 0.15638 | 0.2090 |

| Profit Margin: % | 16.2 | 15.638 | 20.897 |

*See Details in Appendix

As you can see the profit margin has increased for feet and knee but not hip. This looks like a better way of apportioning costs because the number of budgeted operations for knee and feet are more than hip.

Now, let us try to understand what is happening here. Current option apportions or gives indirect costs to each cost element based on budgeted operations. Hip operation and feet operation are allocated less cost. Thus, in one case it is over absorbed but for the other two it is under absorbed.

That is why the net profit margin shows a remarkable fluctuation and it seems certainly that option 2 is better than current option.

In this costing method, the organization looks at what drives the cost. Hence, the activity that drives cost must be connected with the relevant cost.(BPP Learnig Media, June 2009)………

Recent Comments